A Return to ‘Normal’? The State of Real Estate in 2022

Last year was one for the real estate history books. The pandemic helped usher in a buying frenzy that caused home prices to soar nationwide by a record 19.9% between August 2020 and August 2021.1

However, there were signs in the fourth quarter that the red-hot housing market was beginning to simmer down. In the month of October, only 60.3% of sales involved a bidding war—down from a high of 74.5% in April.2 While this trend could be attributed to seasonality, it could also be a signal that the real estate run-up may have passed its peak.

So what’s ahead for the U.S. housing market in 2022? Here’s where industry experts predict the market is headed in the coming year.

MORTGAGE RATES WILL CREEP UP - the current 30 Year Mortgage Rate is 3.7% as of 1/19/2022

Most economists expect to see mortgage rates gradually rise this year after hitting record lows in late 2020 and early 2021.3

Freddie Mac forecasts the 30-year fixed-rate mortgage will average 3.5% in 2022, up from around 3% in 2021.4

The Mortgage Bankers Association predicts that rates will tick up to 4% by the end of the year. "Mortgage lenders and borrowers should expect rising mortgage rates over the next year, as stronger economic growth pushes Treasury yields higher," said Mike Fratantoni, chief economist for the Mortgage Bankers Association at their 2001 Annual Convention & Expo in October.5

However, it’s important to keep in mind that even a 4% mortgage rate is low when compared to historical standards. According to industry trade blog The Mortgage Reports, “Between 1971 and December 2020, 30-year mortgage rates averaged 7.89%.”6

What does it mean for you? Low mortgage rates can reduce your monthly payment and make homeownership more affordable. Fortunately, there’s still time to lock in a historically-low rate. Whether you’re hoping to purchase a new home or refinance an existing mortgage, act soon before rates go up any further. We’d be happy to connect you with a trusted lending professional in our network.

THE MARKET WILL BECOME MORE BALANCED

In 2021, we experienced one of the most competitive real estate markets ever. Fears about the virus and a shift to remote work triggered a huge uptick in demand. At the same time, many existing homeowners delayed their plans to sell, and supply and labor shortages hindered new construction.

This led to an extreme market imbalance that benefitted sellers and frustrated buyers. According to George Ratiu, director of economic research at Realtor.com, “Prices and sellers reached for the moon [last] year. It looks like we are now about to move back to earth.”7

Data from Realtor.com released in November showed that listing price reductions had more than doubled since February 2021. And the average days on market (an indicator of how long it takes a home to sell) has been slowly creeping up since June.7

What’s causing this change in market dynamics? The real estate market typically slows down in the fall and winter. But economists also suspect a fundamental shift in supply and demand.

At the National Association of Realtors’ annual conference last November, the group’s chief economist, Lawrence Yun, told attendees that he expects increased supply to come from an uptick in new construction—which is already underway—and an end to the mortgage forbearance program. “With more housing inventory to hit the market, the intense multiple offers will start to ease,” he said.8

Demand is also predicted to wane slightly in the coming year. Rising mortgage rates and record-high prices have made homeownership unaffordable for a growing number of Americans. And in a recent Reuters poll, nearly 80% of property analysts said they expect housing affordability to worsen over the next several years.9

What does it mean for you? If you struggled to buy a home last year, there may be some relief on the horizon. Increased supply and softening demand could make it easier to finally secure the home of your dreams. If you’re a seller, it’s still a great time to cash out your big equity gains! And with more inventory on the market, you’ll have an easier time finding your next home. Reach out for a free consultation so we can discuss your specific needs and goals.

HOME PRICES LIKELY TO KEEP CLIMBING, BUT AT A SLOWER PACE

Nationally, home prices rose an estimated 16.8% in 2021.8 But the average rate of appreciation is expected to slow down in 2022.

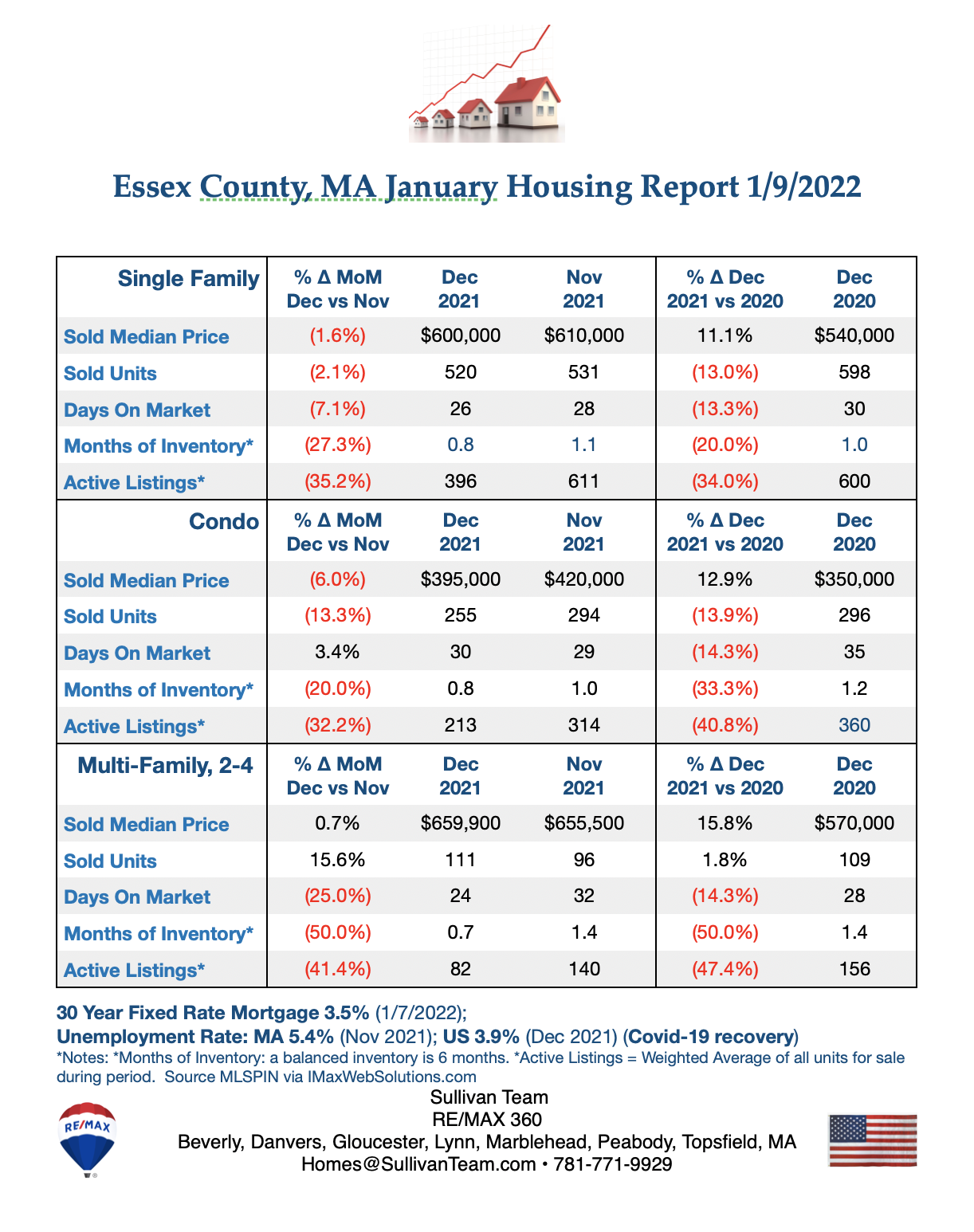

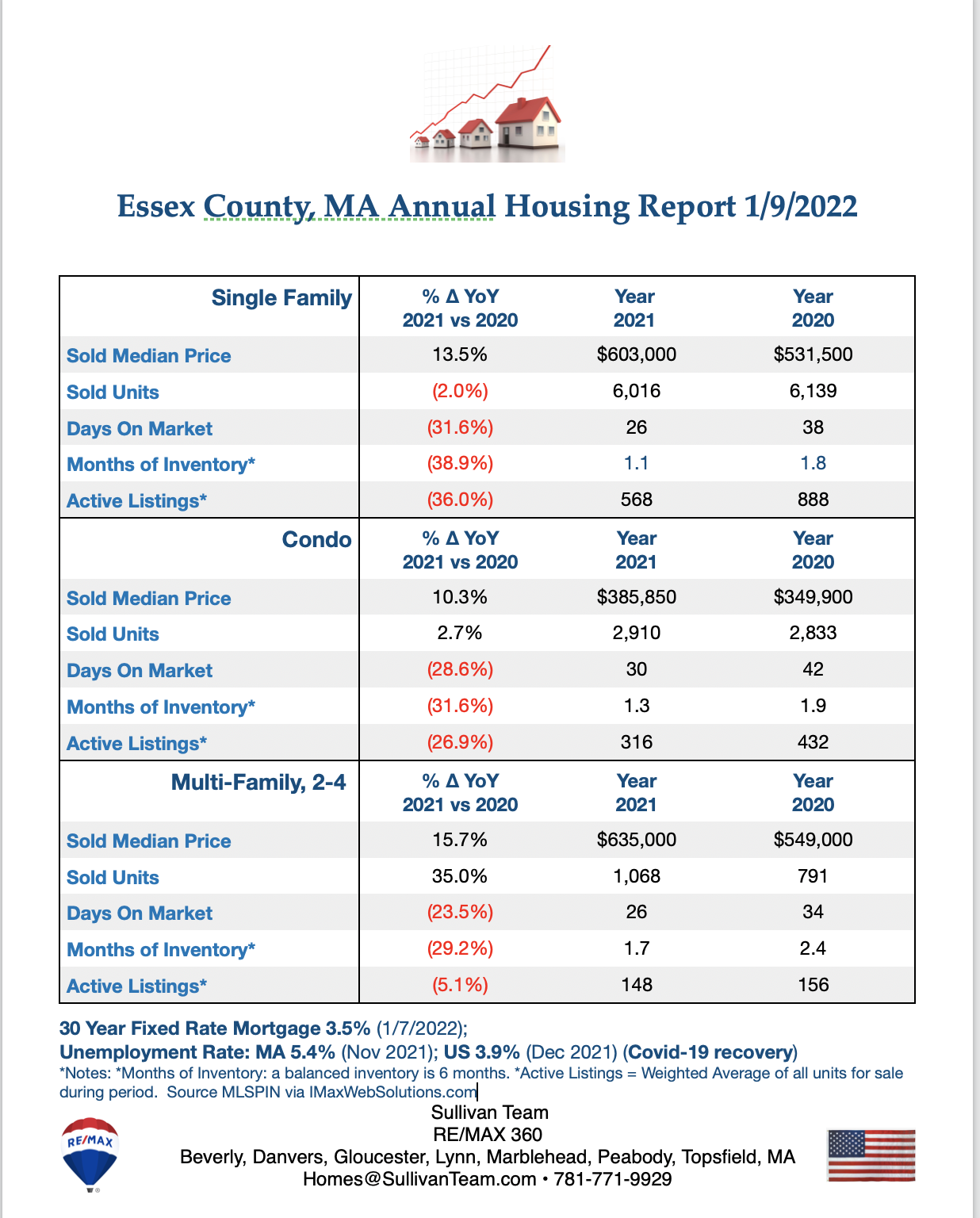

Essex County 2021 prices rose 13.5% for Single Family Homes, 10.3% for Condos and 15.7% for 2-4 Families.

Danielle Hale, chief economist at Realtor.com, told Yahoo! News, “Home asking prices have decelerated in the second half of 2021, with median listing price growth slipping from a peak of 17.2% in April to just 8.6% in October.”10

But experts disagree about how much more property values can continue to climb this year. Goldman Sachs predicts that home prices will rise by 13.5%, while Fannie Mae and Freddie Mac are forecasting a 7.9% and 7% rate of appreciation, respectively.2

However, not all analysts are as bullish. The National Association of Realtors predicts a 2.8% rate of appreciation for existing homes and 4.4% for new homes, while the Mortgage Bankers Association expects the average home price to decrease by 2.5% by the end of the year.10,2

According to Hale, “With prices near all-time highs and mortgage rates expected to rise, we expect this slowdown in prices to continue.”10

What does it mean for you? If you’re a buyer who has been waiting on the sidelines for home prices to drop, you may be out of luck. Even if home prices dip slightly (and most economists expect them to rise) any savings are likely to be offset by higher mortgage rates. The good news is that decreased competition means more choice and less likelihood of a bidding war. We can help you get the most for your money in today’s market.

RENTS WILL CONTINUE TO RISE

Along with home, gasoline, and used vehicle prices, rent prices rose dramatically last year. According to CoreLogic, in September, rents for single-family homes were up 10.2% nationally year over year.11 And economists at Realtor.com expect them to climb another 7.1% in 2022.12

“Homes are expensive now...but for most people, the comparison that is most important is how that cost of homeownership is going to compare to the cost of renting,” Zillow Senior Economist Jeff Tucker told CNBC in November.13

Tucker also pointed out that rent is less predictable than a mortgage—and more likely to go up along with inflation.13

Real assets, like real estate, are often used as a hedge against inflation. That’s because property values typically rise with inflation.14 And when a homeowner takes out a mortgage, they lock in a set housing payment for the next 30 years.

In contrast, renters are at the mercy of the market—and they don’t gain any of the benefits of homeownership, like tax deductions, equity, or appreciation.

George Ratiu of Realtor.com told CNBC that he advises buyers to consider their budget and time frame. If they plan to stay in the home for at least three to five years, he believes it often makes sense to buy.13

Fortunately, it’s shaping up to be a better year for buyers. “I think 2022 has the promise of providing less competition, a lot more homes to choose from, and, as a result, a lot more approachable prices,” Ratiu said.13

What does it mean for you? Both property and rent prices are expected to continue rising. But when you purchase a home with a fixed-rate mortgage, you can rest assured knowing that your monthly mortgage payment will never go up. Whether you’re a first-time homebuyer or a real estate investor, we can help you make the most of today’s real estate market.

WE’RE HERE TO GUIDE YOU

While national real estate numbers and predictions can provide a “big picture” outlook for the year, real estate is local. And as local market experts, we can guide you through the ins and outs of our market and the local issues that are likely to drive home values in your particular neighborhood.

If you’re considering buying or selling a home in 2022, contact us now to schedule a free consultation. We’ll work with you to develop an action plan to meet your real estate goals this year.

Sources:

- Fortune -

https://fortune.com/2021/11/04/us-home-prices-real-estate-forecast-2022-outlook/ - Fortune -

https://fortune.com/2021/11/29/housing-market-real-estate-predictions-2022-forecast/ - Freddie Mac -

http://www.freddiemac.com/pmms/pmms30.html - Freddie Mac - https://freddiemac.gcs-web.com/news-releases/news-release-details/freddie-mac-strong-housing-market-will-continue-even-rates-and

- Mortgage Bankers Association -

https://www.mba.org/2021-press-releases/october/mba-annual-forecast-purchase-originations-to-increase-9-percent-to-record-173-trillion-in-2022 - The Mortgage Reports -

https://themortgagereports.com/61853/30-year-mortgage-rates-chart - Realtor.com -

https://www.realtor.com/news/trends/has-housing-market-peaked/ - National Association of Realtors -

https://www.nar.realtor/newsroom/nars-yun-says-housing-market-doing-well-may-normalize-in-2022 - Reuters -

https://www.reuters.com/world/us/rise-us-house-prices-halve-next-year-affordability-worsen-2021-12-07/ - Yahoo! News -

https://www.yahoo.com/now/where-home-prices-headed-2022-130012748.html - CNBC -

https://www.cnbc.com/2021/11/16/inflation-rent-for-single-family-homes-surged-10percent-in-september.html - Realtor.com -

https://www.realtor.com/news/trends/what-to-expect-in-2022-housing-market/ - CNBC -

https://www.cnbc.com/2021/11/23/rising-inflation-hot-housing-market-what-you-need-to-know-about-buying-a-home.html - Money -

https://money.com/inflation-2021-stocks-bitcoin-gold-reits-commodities/