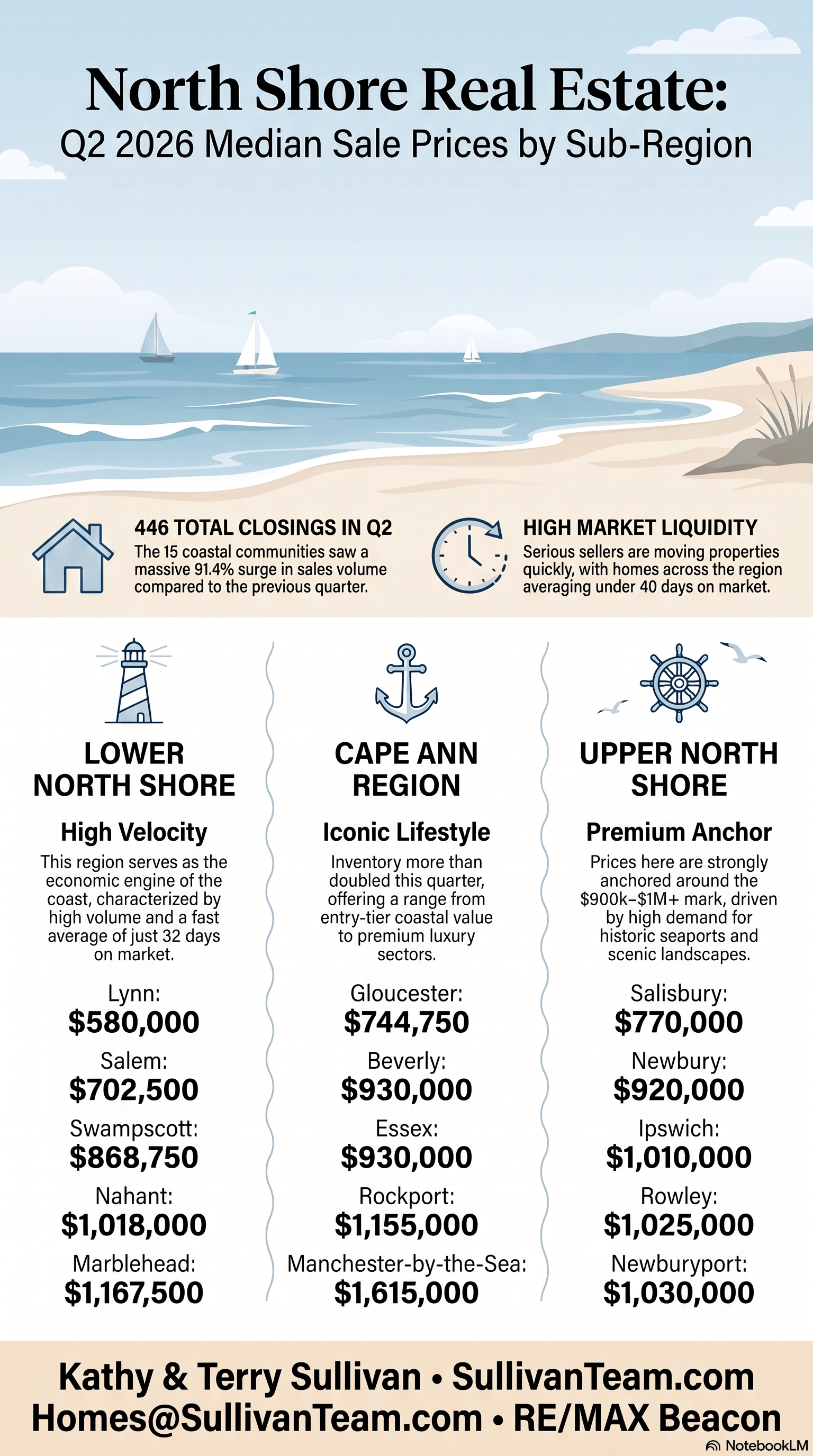

The real estate landscape across the Essex County coast has reached a fever pitch in 2026. Data from the second quarter reveals a 91.4% surge in market activity across the 15 coastal communities, with 446 single-family homes closing during this period. At the heart of this activity is the Lower North Shore, a region often described as the "high-velocity economic engine of the coast".

Whether you are looking for urban energy, historic charm, or secluded seaside living, the five primary cities of the Lower North Shore—Lynn, Nahant, Swampscott, Marblehead, and Salem—offer distinct opportunities for residents. With market liquidity at an all-time high and homes in this region moving at an average speed of 35 days on market, understanding the nuances of each community is essential for a successful transition.

For expert guidance navigating these trends, the Sullivan Team provides over 70 years of combined experience to help you find the perfect match.

1. Lynn: The High-Velocity Economic Engine

Lynn stands as a powerhouse of the region, leading the Lower North Shore in sales volume with 88 single-family properties sold in Q2 2026. This city offers a dynamic environment with deep historic roots and a growing modern infrastructure.

Why Move to Lynn? Lynn is an ideal choice for those who value accessibility and a vibrant, urban-suburban atmosphere. The city features the sprawling Lynn Woods Reservation, one of the largest municipal parks in the United States, offering miles of trails for hiking and recreation. Residents also enjoy proximity to Lynn Shore Drive, a scenic coastal promenade perfect for seaside walks.

- Q2 2026 Median Sale Price: $580,000.

- Market Speed: 38 days on market.

- Key Amenities: Lynn Woods Reservation, waterfront access via Lynn Shore Drive, diverse culinary scene, and reliable commuter rail access to Boston.

- Search Lynn Homes: View available listings in Lynn.

2. Nahant: The Secluded Coastal Enclave

Nahant is a unique coastal community that offers a sense of seclusion while remaining remarkably close to the regional hubs. Connected to the mainland by a narrow causeway, it provides a specialized lifestyle for those seeking an island-like atmosphere.

Why Move to Nahant? Nahant is characterized by its stunning natural beauty and maritime heritage. Life here revolves around the ocean, with Short Beach and Long Beach serving as primary recreational anchors. The community is focused on preserving its scenic vistas and quiet residential character, making it a premier destination for those who appreciate tranquility and open water views.

- Q2 2026 Median Sale Price: $1,018,000.

- Market Status: A premium market with high demand for limited inventory.

- Key Amenities: Scenic beaches (Short and Long Beach), the historic Lodge Park, and breathtaking views of the Boston skyline from the southern cliffs.

- Search Nahant Homes: Explore Nahant seaside properties.

3. Swampscott: Suburban Coastal Elegance

Swampscott seamlessly blends the comforts of a classic suburban community with the undeniable allure of the Atlantic. It is known for its well-maintained seaside parks and a refined yet welcoming atmosphere.

Why Move to Swampscott? Residents are drawn to Swampscott for its high level of community engagement and scenic public spaces like Linscott Park and the Swampscott Fish House. The town offers a balanced pace of life, where one can enjoy a quiet morning by the water followed by a quick commute into the city. Its market remains competitive, with serious buyers and sellers finding success in a high-liquidity environment.

- Q2 2026 Median Sale Price: $868,750.

- Market Speed: 35 days on market.

- Key Amenities: Beautiful seaside parks, the historic Fish House, local boutique shopping, and direct commuter rail connections.

- Search Swampscott Homes: Browse Swampscott real estate.

4. Marblehead: The Premium Coastal Icon

Marblehead is widely recognized for its deep nautical history and its status as a premium anchor of the North Shore. In Q2 2026, it saw a significant 34.9% increase in median sale prices, highlighting its enduring desirability.

Why Move to Marblehead? Marblehead is a global destination for sailing enthusiasts and lovers of colonial history. The Old Town district features narrow, winding streets lined with 17th and 18th-century architecture, while Marblehead Neck offers some of the most impressive waterfront estates in the region. The town's harbors are central to its identity, providing endless opportunities for boating and coastal recreation.

- Q2 2026 Median Sale Price: $1,167,500.

- Market Speed: An incredibly fast 23 days on market.

- Key Amenities: Marblehead Harbor, the historic Old Town district, Castle Rock Park, and prestigious yacht clubs.

- Search Marblehead Homes: View premium Marblehead listings.

5. Salem: The Cultural Hub of the North Shore

Salem is more than just a historic destination; it is a thriving cultural and economic center with a robust residential market. With 40 homes sold in Q2 2026, Salem continues to be a high-volume leader in the region.

Why Move to Salem? Salem offers an unmatched blend of history, culture, and modern amenities. The downtown area is highly walkable, featuring the world-renowned Peabody Essex Museum, a wide array of fine dining, and a vibrant arts scene. Its diverse housing stock ranges from historic Federal-style mansions to modern condominiums, providing options for a wide variety of lifestyle preferences.

- Q2 2026 Median Sale Price: $702,500.

- Market Speed: 30 days on market.

- Key Amenities: The Peabody Essex Museum, the historic Salem Maritime National Historic Site, a walkable downtown, and a seasonal ferry to Boston.

- Search Salem Homes: Find your place in historic Salem.

Navigating the Lower North Shore Market

The data is clear: the Lower North Shore is moving fast. With median prices ranging from $580,000 in Lynn to over $1.16 million in Marblehead, there is a specialized segment for every serious buyer. However, in a market where properties often move in under 40 days, having an experienced team is vital.

Kathy and Terry Sullivan have lived on the North Shore since 1982 and have helped over 1,765 clients navigate these local markets. Their hyper-local strategy and extensive professional designations—including Certified Luxury Home Marketing Specialist (CLHMS) and Pricing Strategy Advisor (PSA)—ensure that you are positioned for success whether you are buying or listing.

Take the Next Step

Are you ready to explore the possibilities on the Lower North Shore? Contact us today to discuss a custom strategy for your real estate goals.

Kathy Sullivan & Terry Sullivan RE/MAX Beacon Kathy: 781-771-9949 | Terry: 781-771-9929 Email:Kathy@SullivanTeam.com | Terry@SullivanTeam.com Website: www.SullivanTeam.com

Meta Description: Compare the Q2 2026 real estate trends for Lynn, Nahant, Swampscott, Marblehead, and Salem. Discover median prices, city amenities, and why the Lower North Shore is the high-velocity economic engine of the coast.

Keywords: Lower North Shore Real Estate, Lynn MA Median Price, Marblehead Homes for Sale, Salem MA Real Estate Trends, Swampscott Coastal Living, Nahant Real Estate, Sullivan Team North Shore, Q2 2026 Market Report Essex County.